Trading with VWAP – Glorified moving average or good trading strategy?

In this article, we will take a look at the Volume-weighted average price (VWAP).

VWAP is a popular trading tool.

It is often referred to as something that big institutional and banks are using in their trading and because of that, you must use it in your trading as well.

Since probably one of the best things you can do in trading is being skeptical about everything you hear or read.

Instead of starting using a VWAP right away, you should take a deep look into what VWAP is and if it is worth to use it.

And that is exactly what I will show you in this article, after covering the basics first, we will have a look at different variations and use cases of VWAP so after you will finish reading this article, you might have a better judgment if VWAP really is something useful or not.

If you like this article, read the rest of the blog or join the Tradingriot Bootcamp for a comprehensive video course, access to private discord and regular updates.

For those who are looking for a new place for trading crypto, make sure to check out Woo. If you register using this link and open your first trade, you will get a Tier 1 fee upgrade for the first 30 days, and we will split commissions 50/50, which means you will get 20% of all your commissions back for a lifetime. On top of that, you will receive a 20% discount for Tradingriot Bootcamp and 100% free access to Tradingriot Blueprint.

You can either read the blog post or watch video version on youtube:

Table of Contents

What is Volume-Weighted Average Price (VWAP)?

Compared to the simple moving average which only takes into consideration candle closes by a given period of time.

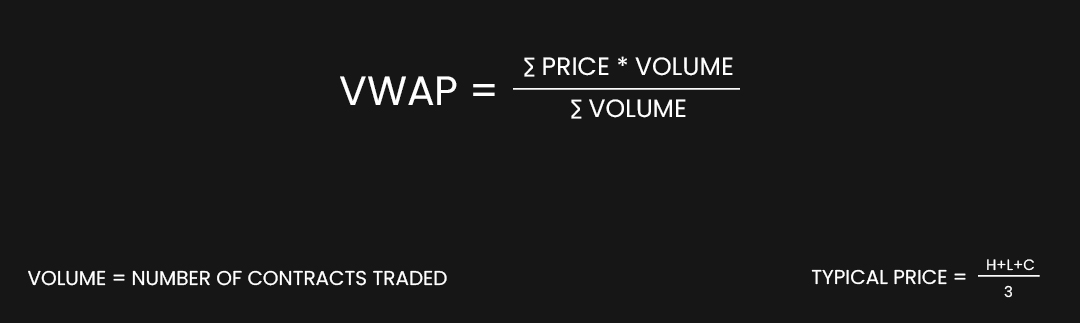

VWAP incorporates volume into the calculation.

For those that are interested he is the actual formula of how VWAP is calculated.

This is actually a great way to look at an average price since the Volume measures the success or failure of the auction which is one of the key pillars of the Auction Market Theory.

Moving average vs Volume Weighted Average Price

To better understand the advantage of VWAP over a simple moving average, let’s have a look at a practical example.

Imagine that you have 1000 contacts traded at four different prices.

- 100 contracts were traded at a $98 price point

- 100 contracts were traded at a $99 price point

- 700 contracts were traded at a $100 price point

- 100 contracts were traded at a $101 price point

If we plot a simple moving average, we will get a value of $99,5 which are all price points divided by four.

If we want to calculate the VWAP value, we have to add a number of contracts traded as they represent the Volume.

Remember the calculation is (Price*Volume)/Volume.

- 98 * 100 = 9800

- 99 * 100 = 9900

- 100 * 700 = 70000

- 101 * 100 = 10100

All we have to do now is divide the total number of Price * Volume by Volume.

VWAP = 99800 / 1000 = $99,8

As you can see there is a $0.30 difference between the moving average and VWAP.

It is simply because VWAP puts more weight into the price points where more volume was traded

Here you can see a VWAP and 48-period Simple Moving Average plotted on a chart of Bitcoin.

As this is a 30-minute chart, those 48 periods represent 24 hours.

The difference between moving average and VWAP is the fact that VWAP resets at the start of a new day, therefore we can use a Rolling VWAP which we cover later on.

VWAP – an institutional trading strategy?

If you have ever seen any youtube video or read an article about VWAP, one of the first sentences is that VWAP is used by large players in the market and how you must use it as well.

Like the ClayTrader in his video modestly called Why I Started Using This Day Trading Indicator (the best!).

In the video which has over 500,000 views, he pretty describes VWAP as a tool used by portfolio managers and how they see a VWAP as a fair value.

Therefore when the price is below VWAP, they buy the underlying asset and when the price is above VWAP, they sell the underlying asset so they get more favorable prices for their clients.

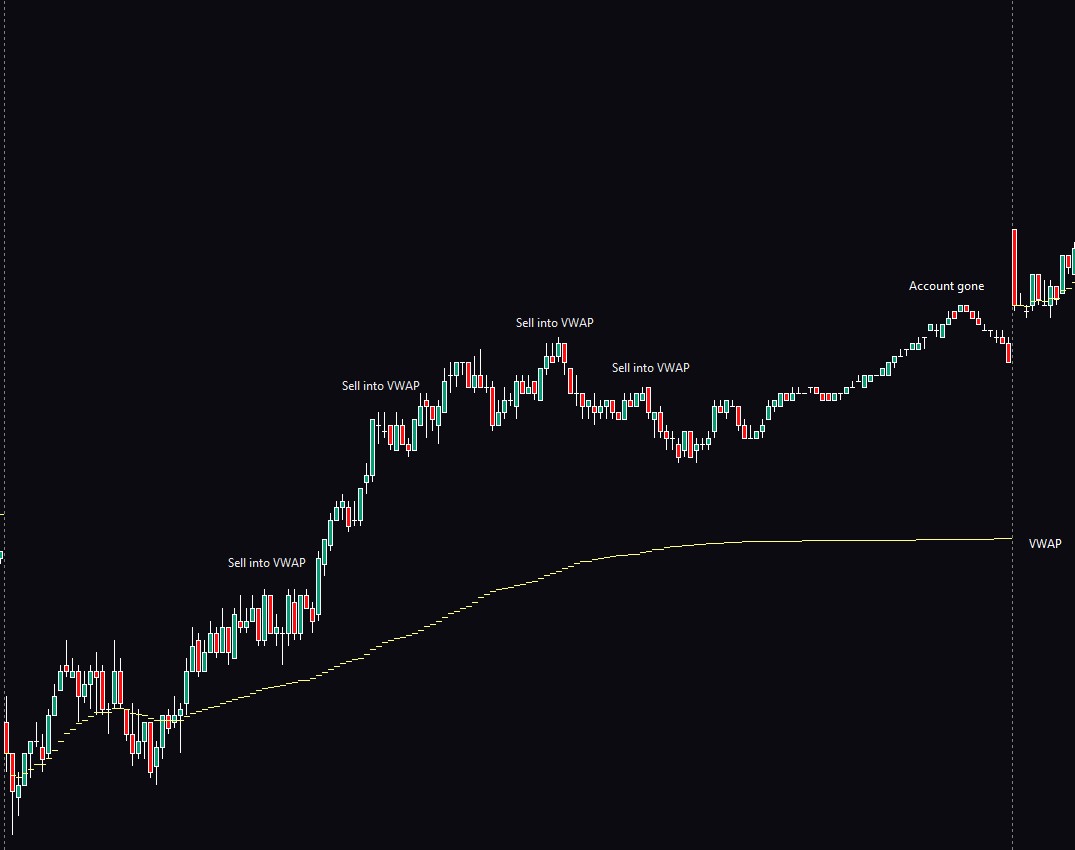

Coming into the market with this mindset, all you need is one trend day to blow your account.

Although mean reverting with VWAP can work, it should never be used as a standalone strategy.

Because of the “Institutional” indicator, you will find a lot of other videos with quite a lot of views about VWAP.

Some will tell you to fade moves into VWAP and some will use VWAP as a trend indicator for continuation once price breaks above/below VWAP.

Before I show you the way how to use both, let’s cover the topic of large players trading with the VWAP.

Although it is true and you can find plenty of resources of VWAP being used by large traders and also algorithms.

You can never know how these people and bots use VWAP in decision making.

Therefore, it is completely useless to make some huge assumptions based on VWAP and justify our trading decision with this whole “institution trading approach”, simply because you never know what someone on the other side of the screen about to do.

With that being said, VWAP is a valuable tool and when used properly, it can bring great results.

VWAP Trading Strategy

Instead of trying to play a mean reversion, more often than not is much easier to follow established trends in the market.

Using a VWAP as a trend trading tool is extremely simple and effective.

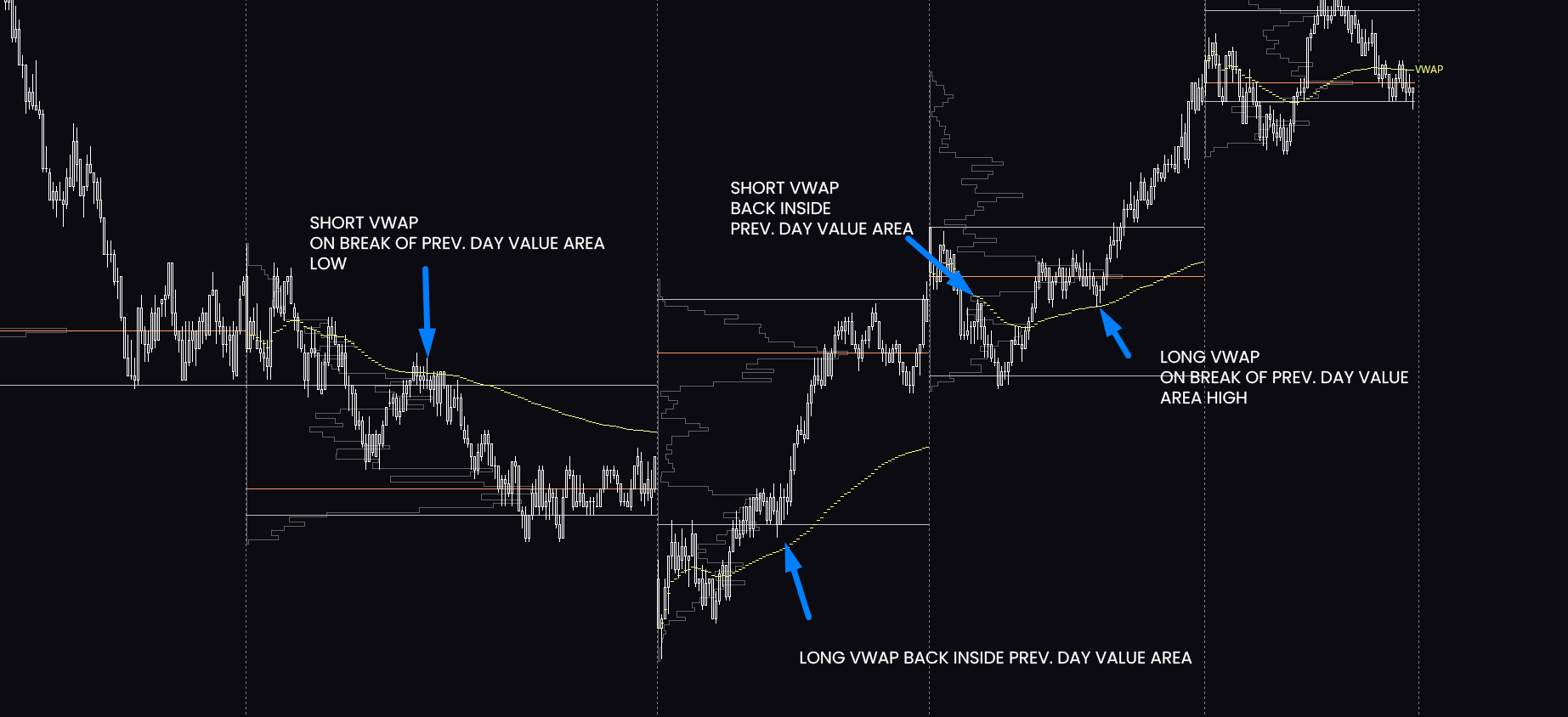

- For buying, you wait for a break and retest above VWAP for a day

- For selling, you wait for a break and retest below VWAP for a day

A disadvantage of this approach is that VWAP is similar to other Volume-based tools, Point of control.

This means that same as a point of control it is an area with high executed volume, therefore prices can get much more range-bound before move one way or another.

But using something as simple as a Volume profile can add much more confluence to our ideas when we are trading with VWAP.

If you are not aware of how to trade with Volume profile, go and check out this article.

With an understanding of the Auction Market Theory and Volume Profiling method, we can easily add a filter to VWAP trading which will give us much higher accuracy.

I also use several price action and orderflow patterns which can highly increase the probability of these trades, these are shown in the Trading Blueprint.

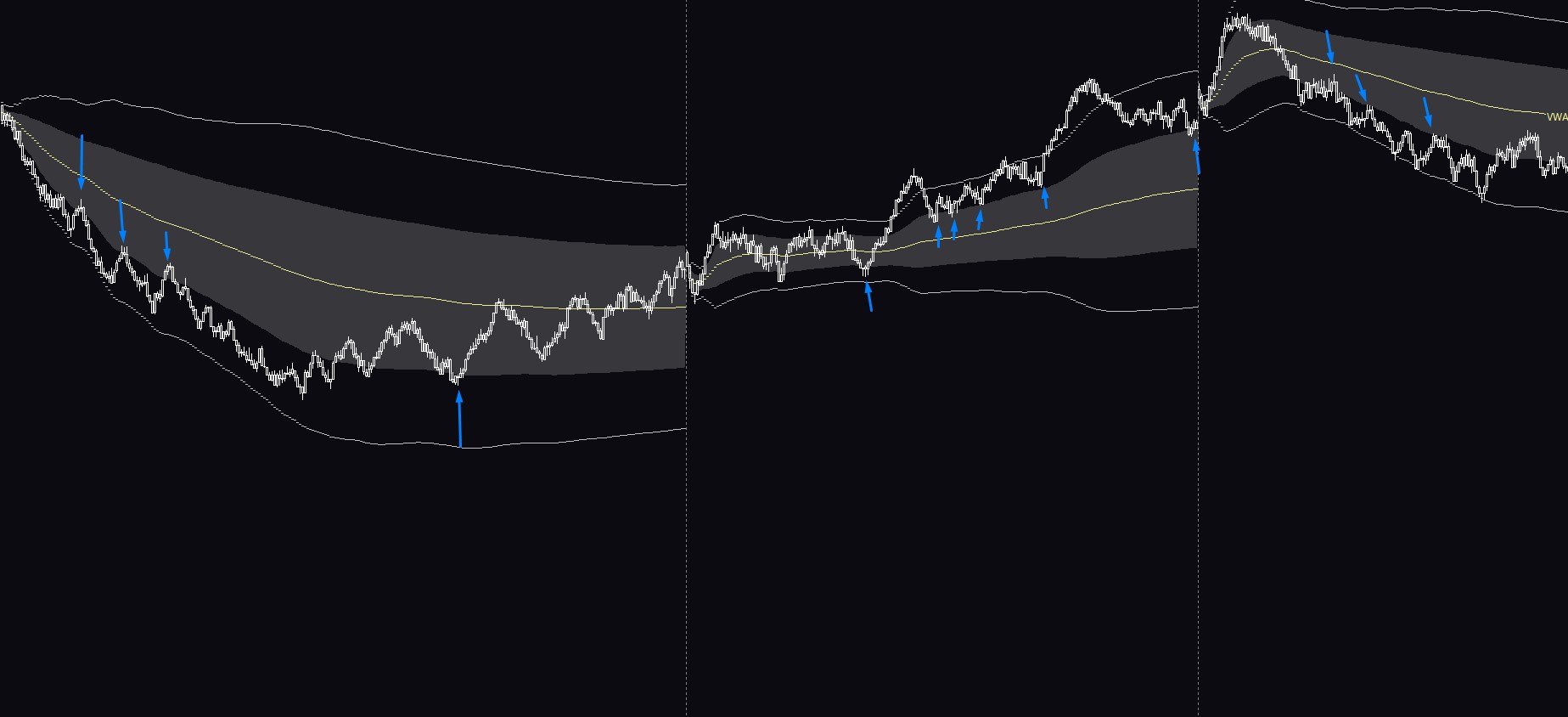

VWAP Standard Deviation Bands

As I already mentioned, using any mean-reverting strategy such as Bollinger Bands, Keltner Channels, or VWAP Standard Deviation Bands can be risky business.

If you will try to mean revert everything, it only takes one trend day and you can cause huge damage to your account.

That being said, there is a great use with these VWAP bands.

Not only for mean reversion but also trend following as we can latch into the move using 1 or 2 standard deviations of VWAP.

As you can see in the picture above, the grey shaded area represents 1 standard deviation of VWAP, and the line above/below shows 2 standard deviations of VWAP.

On strong trending moves, the price oftentimes does not pull back all the way to VWAP therefore we can latch to the move using the 1 std. deviation band.

Once price accepts back inside that one standard deviation range, we can take a trade targeting VWAP or the other side of the band.

Although mean reverting back to VWAP can work well, using VWAP in a trend following fashion is oftentimes the easier trade as all you need is breakout and retest.

When I mean revert back into VWAP, I tend to be much more careful and look for many more factors of confluence compared to simple break and VWAP retest.

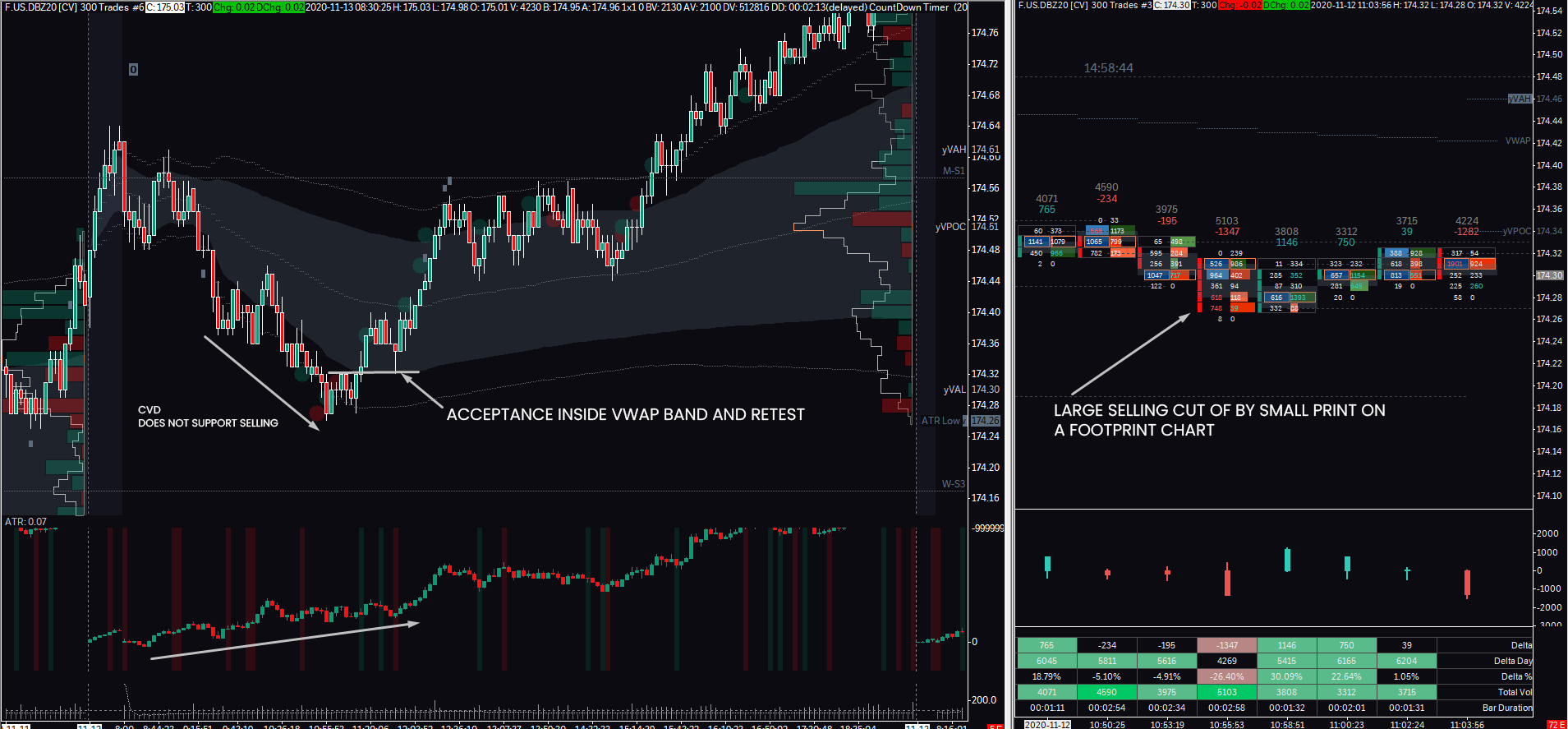

As you can see with this example, the long opportunity at 1 standard deviation band of VWAP, was strongly supported by orderflow confluence in the Cumulative Volume Delta and Footprint chart.

VWAP Swing Trading Strategy

Now as we covered the basics of VWAP and how it can be utilized for intraday trading, let’s have a look at how we can use VWAP for swing trading.

There are three types of VWAPs we can use for a swing trade, each of them has their pros and cons.

Fixed Time Periodicity VWAP

Same as in intraday trading VWAP measures one trading day (or trading session), we can plot a VWAP that starts a new week, month, quarter, or year.

These VWAPs simply show us Volume weighted average price for a fixed time period and their best use-case can be found in trending environments.

The obvious disadvantage of using these is the fact that they will pretty much flat once the new period start.

So if you use weekly VWAP, you won’t get much data on Monday same as if you use yearly VWAP, you won’t get much data in January.

Rolling VWAP

The Rolling VWAP solves the problem of VWAP with fixed time periodicity as it continuously rolls based on a fixed time period.

This is an especially useful tool if you are trading a Bitcoin or other cryptocurrencies where the market doesn’t close over the weekend.

So instead of weekly VWAP that will reset every Monday and start with the first bar at midnight, rolling VWAP will continue its trajectory factoring the Volume Weighted Average Price of last 7 days.

The same can be used on an intra-day basis where we can use a 1-Day rolling WVAP as more of a trend-following tool which is not based on a fixed time start.

Anchored VWAP

The last VWAP we can use for capturing larger swings in the market is Anchored VWAP which eliminated time completely.

Because of that, you can anchor VWAP at any place on the chart you want.

This opens door to go a little crazy with the Anchored VWAP.

If I can give you a piece of advice, these Anchored VWAPs work best when they are anchored to key daily and weekly swing points.

Once we anchor these VWAPs on the higher timeframes, we can switch to lower ones for little more detailed view.

Conclusion

Since Volume is averaged into VWAPs calculation, it makes it a great tool to use in your trading.

Although the fact that you are using something which is also utilized by funds and algos might help you sleep at night, VWAP is still a lagging indicator that simply shows you a moving average based on price and volume.

This is why it’s important to not use this indicator blindly, but as a confluence tool for your already existing trading ideas.

If utilized properly, VWAP can bring a great amount of confluence to your trading strategy.