Understanding futures, options and other derivatives

One of the most mind-boggling things I see from people coming into trading is that they have no idea what they are trading.

Not understanding the market you trade can create various problems, especially when the position goes against you.

This article will cover the basics of the most popular derivatives you will find out in crypto and legacy markets.

If you like this article, read the rest of the blog or join the Tradingriot Bootcamp for a comprehensive video course, access to private discord and regular updates.

For those who are looking for a new place for trading crypto, make sure to check out Woo. If you register using this link and open your first trade, you will get a Tier 1 fee upgrade for the first 30 days, and we will split commissions 50/50, which means you will get 20% of all your commissions back for a lifetime. On top of that, you will receive a 20% discount for Tradingriot Bootcamp and 100% free access to Tradingriot Blueprint.

Video version of the article.

Table of Contents

What is a derivative?

A derivative is a contract that derives its value from an underlying asset.

First mentions about derivatives date back to ancient Greek, where a derivative contract was used in trading olives.

More recent history and the rise of the popularity of derivatives can be found in the 1930s where Bucket shops used derivatives.

Derivatives can be created from any underlying asset, Stocks, Bonds, Cryptocurrencies, commodities, etc.

The derivatives market is genuinely enormous; according to European Securities Market Authority, in 2017, estimated the size of the European derivatives market was €660 trillion with 74 million outstanding contracts.

There are two main ways how derivatives are traded.

Privately Over-the-counter (OTC) and exchange-traded derivatives (ETD).

Derivatives are used in two major ways.

- Hedging purposes are usually used by larger players.

- Speculation and arbitrage are usually used by smaller/retail traders

This simple example of derivative and one of the most popular ones is the E-Mini S&P500 futures contract which has underlying in Standard & Poor’s 500 stock index.

Futures

What is a futures contract?

A futures contract is a legal agreement to buy or sell a pre-determined amount of financial instrument at a specified price at a specified date in the future.

Before futures became the main instrument of speculators, they were and still are used as hedging instruments.

For example price of Coffee futures that expire in March 2025 is currently at approximately $225.

If you have a company that sells coffee and doesn’t want to expose themselves to price fluctuations as they think $225 is a fair price for their coffee, they can sell March futures at $225.

This gives them the obligation to deliver a specified amount of Coffee futures at the March expiration date.

But no need to worry; you won’t be obligated to deliver physical coffee or oil at the expiration date.

As futures become more and more popular for speculations, futures brokerages prevent physical delivery by closing your positions at rollover dates (rollover = when volume moves from expired futures contract to next month.)

Each futures contract has its specific code.

The E-mini S&P500 is the most popular and traded futures contract globally.

If we look at the contract that is traded right now, you will see that it’s called ESH2022.

As letters ES (name of the contract) and 2022 (year of the expiration) sound relatively straightforward, the letter H can be quite confusing.

The letter H stands for the month of the expiration; in this case, that is March.

Other expiration months go as follow:

- January – F

- February – G

- March – H

- April – J

- May – K

- June – M

- July – N

- August – Q

- September – U

- October – V

- November – X

- December – Z

Expiration also differs based on the contract.

Most futures contracts like index futures or cryptocurrencies expire quarterly, but some commodity futures contracts like Crude Oil expire every month.

Legacy futures

This article aims not to cover every futures contract separately, and I did that here.

The legacy futures market is huge and spread across different venues that offer different products worldwide.

The most famous futures exchange is CME Group, offering index futures such as E-Mini S&P500, Nasdaq, or Dow Jones.

Besides that, you can also trade currency futures or cryptocurrency futures, namely Bitcoin and ETH.

Other popular venues are CBOT which is the partner organization of the CME group and offer mostly Bond futures.

Commodities such as Gold, Siler, Natural Gas or Crude Oil are traded at Nymex and Comex.

Outside of the US, there are exchanges such as ICE, Eurex, MOEX, Osaka Exchange, etc.

The products by themselves differ based on sizes, expiration dates, or trading hours.

What always stays the same is the underlying principle of futures and the fact all these futures expire.

Cryptocurrency Perpetual Futures

Perpetual futures contracts (also called perpetual swaps) became the most popular futures contracts after Bitmex introduced them in 2016.

Although most people think they were created especially for the cryptocurrency market, it is not true.

They appeared first in 1992, created by Robert Shiller to bring futures to illiquid assets.

Nowadays, they are an inseparable part of the cryptocurrency market; there has been an attempt to introduce “deliverable” futures contracts by an exchange called Coinflex, but it never really caught up.

Like index futures, cryptocurrencies settle in cash; the only difference is that perpetual swaps don’t have an expiration date.

Since these perpetual contracts don’t expire, traders pay or receive a fee in regular hourly windows; this dynamic is called funding rate.

Funding rates

When Bitmex introduced perpetual swaps, they also created a never-ending cycle of an 8-hour time window where they started charging interest rates based on a premium discount of swap contract and underlying price of Bitcoin.

The funding fee is exchanged directly between buyers and sellers every 8 hours.

- When the funding rate is positive, long position holders pay short position holders.

- When the funding rate is negative, short position holders pay long position holders.

The amount differs based on your position size and the calculation looks like this:

Funding fee = position value * funding rate

If funding is negative, the swap was trading below (at the discount) against the spot and shorts have to pay a fee to longs.

If funding is positive, it means that the swap was trading above (at the premium) against the spot and longs have to pay a fee to shorts.

Most of the time, this is directly correlated with the direction the market is heading. Funding works as a mechanism to incentivize traders to open counter-trend positions and balance out the order book.

Since we all know retail traders usually tend to be wrong, extremes of funding rates can be used in building a trading strategy.

Prolonged periods of high funding rates can be signals for markets being overbought/oversold.

Funding rates differ based on the exchange; for example, on FTX funding rate happens every hour instead of 8-hours.

Also, if you take a look at perpetual swaps for different altcoins, you might start to think that there is an obvious short squeeze about to happen as the numbers can get quite high.

For example, those who hold short on RAY-Perp on FTX pay a 34% annualized funding rate that is charged to their position every hour.

If you take a look at a chart of RAY-Perp, you would expect it just to go up, but it’s not the case.

Traders are willing to pay high funding on their perpetual swap positions because they use those altcoins to build delta neutral positions and collect yield without directional exposure.

For this example of Ray, it might be single staking at Raydium, although it would be a not profitable trade in the long run as the APR for staking is currently lower than the funding rate on FTX.

Types of cryptocurrency futures contracts

There are two types of futures contracts exchanges offer nowadays, inverse (coin marginated) and USD marginated futures.

USD marginated futures are straightforward; you deposit synthetic USD (usually USDT) to the exchange, and your account balance and equity always stay in USDT.

These futures are more popular as they are offered by exchanges such as Binance, FTX and Bybit.

They are newer products as inverse futures were the first one introduced by Bitmex.

Inverse futures keep your balance in the coin instead of dollars.

This brings another factor traders have to deal with: coin fluctuations by itself.

The most popular exchanges nowadays that offer inverse contracts are Bybit and Bitmex.

Suppose you are interested to learn more about Bitcoin futures and going into the nitty-gritty of the contracts. In that case, I recommend you to read the documentation on the exchanges or Medium posts from Romano and Austerity Sucks as they have plenty of articles about crypto derivatives.

Futures mechanics

Futures are traded on leverage; leverage gives you more buying power than your account has.

Every position requires margin from your side, but the rest is compensated with leverage.

Because you are trading with more money you have, the last thing exchange wants is to pay for your losses.

So if positions go against a certain amount, your trade can get automatically close (liquidated).

If the price of Bitcoin is $10,000 and you will buy 1 BTC with 10x leverage, you are only depositing 10% of the position for the trade, $1,000.

If the price of Bitcoin drops 10% and it is currently at $9,000, your position gets liquidated.

Always be mindful of these things and how leverage can affect your position.

CFDs

What is a CFD?

CFD stands for Contract for Difference, and it is another type of derivative traders can trade.

You will find CFDs offered mainly through Forex brokers as a substitution for futures contracts.

They don’t exactly have the best reputation as Forex brokers run different B-Book models (opening positions against traders) and can essentially widen the spreads of those CFDs.

Of course, if you choose a trusted and regulated broker, you have nothing to worry about.

CFDs vs Futures

As I have already mentioned, CFDs and futures are very similar.

CFDs are also perpetual. Therefore they don’t expire.

Also, if you will look at ESH2022 on the CFD platform, you wouldn’t find it.

CFDs are always under different names as official names by futures exchanges are trademarked, so S&P500 is usually called US500 instead of ES and so on.

There is only one reason to trade CFDs rather than Futures contracts if you are working with a small balance.

One point on E-Mini S&P500 Futures equals $50, on CFDs which is usually only $1 for the smallest positions size.

CFDs are a very niche market that gets a lot of hate often.

They are banned in the US and other parts of the world but offered by many European regulated brokers.

If you have higher capital, I would always suggest you trade the Futures markets, especially with micro contracts available.

Other than that, CFDs can be used to trade thin markets like Nasdaq or Dax where spread does not play a high role or to build a long term position with fewer margin requirements compared to futures where you are forced to deploy more margin for holding outside of regular trading hours.

Options

What are options?

Options give a holder right but not an obligation to buy or sell the underlying asset at a specified price on the specified date.

The buyer of the options pays a premium, seller of the option receives the premium.

To translate this too much more simple terms, let’s say you want to buy a house and find a seller.

You ask the seller if he can issue you an option that expires in 3-months and gives you the right to buy the house for $500,000; he will also receive a premium for this option which equals $10,000.

If he agrees, you have a right to buy a house for $500,000 anytime in those three months, and you don’t need to care about housing market price fluctuations.

Let’s say the three months passed, and the current price of the house is only $450,000.

In this case, you are obviously not going to buy a house for 500k, so you will not exercise your right to buy the house.

But you lost the $10,000 premium, which was the risk you put in.

In another example, let’s say that the housing market skyrocketed, and the current price of that house is now $700,000.

Of course, you are going to exercise your right to buy the house for $500,000, and you made a profit of $190,000 (Final price (700k) – Strike Price (500k) – Premium (10k).

Let’s now flip the table and look at the situation from the perspective of the option seller.

In the first scenario, the option expired worthless as the price of the house was below to option price, and the seller ended up in profit of premium he was paid to.

In the second scenario, the options ended up in the money, and the seller technically lost $190,000 as he now has to sell a house that has a $700,000 value only for $500,000 (minus the premium.)

This principle is the same in options trading as well.

If you are an option buyer, your risk is limited only to the premium paid, and your reward is technically unlimited.

If you are an option seller, your reward is limited only to the premium you receive, and your risk is technically unlimited.

Although this might sound like selling options is the worst idea ever, options are extremely complex derivatives, and things are not as simple as they might seem.

Options basics

So now that you know how options work, it is a great time to translate this knowledge into the markets.

Although the example of buying a house was rather simple, if you open an option chain on a platform such as Deribit, it looks like everything but simple.

When you want to open an order on futures, it is usually very straight forwards, you either buy or sell.

On options chains, there are much more elements to consider.

To make things as simple as possible, you first need to pick up a strike price.

When choosing a strike price, you usually hear three terms that are related to the current price of the underlying asset. You might hear the term “moneyness” of the option.

- In the money (ITM) – Option strike price is “in the money” with the underlying asset. An example of this is you buying January 28th Call with 45000 strike price, and Bitcoin is currently trading at 47000.

- At the money (ATM) – Option strike price is the same as the current price of an underlying. Buying a January 28th Call with a 47000 strike price and Bitcoin trading at 47000 mean you are buying “at the money option”.

- Out the money (OTM) – Option strike price has no intrinsic value compared to underlying. Buying a January 28th Call with a 50000 strike price and Bitcoin trading at 47000 mean you are buying “out of the money option”.

Moneyness is the intrinsic value of an option’s premium in the market.

If you are wondering what intrinsic value is, every option has two values Intrinsic and Extrinsic Value.

The intrinsic value of an option is the value of the option at expiration.

In other words, the 45000 strike price option of underlying that is currently trading at 50000 has an intrinsic value of 5000.

Extrinsic value is also called a time value.

Extrinsic value depends on time to expiration, volatility, dividends and risk-free interest rate of underlying.

If we take a look at two options, one that expires tomorrow and one that expires a month from now.

The option with a longer period of expiration has a higher extrinsic value because it has a longer time to expiration.

Options strategies

When trading options, you will notice the lack of classic “Long” and “Short” buttons you might be used to from other derivatives.

You trade Calls and Puts in options, and you can go both long and short on them.

When you are trading options, you can be either bullish or bearish and make a profit when markets are either not moving or profit on a significant move without being correct in the direction.

Let’s start with simple things.

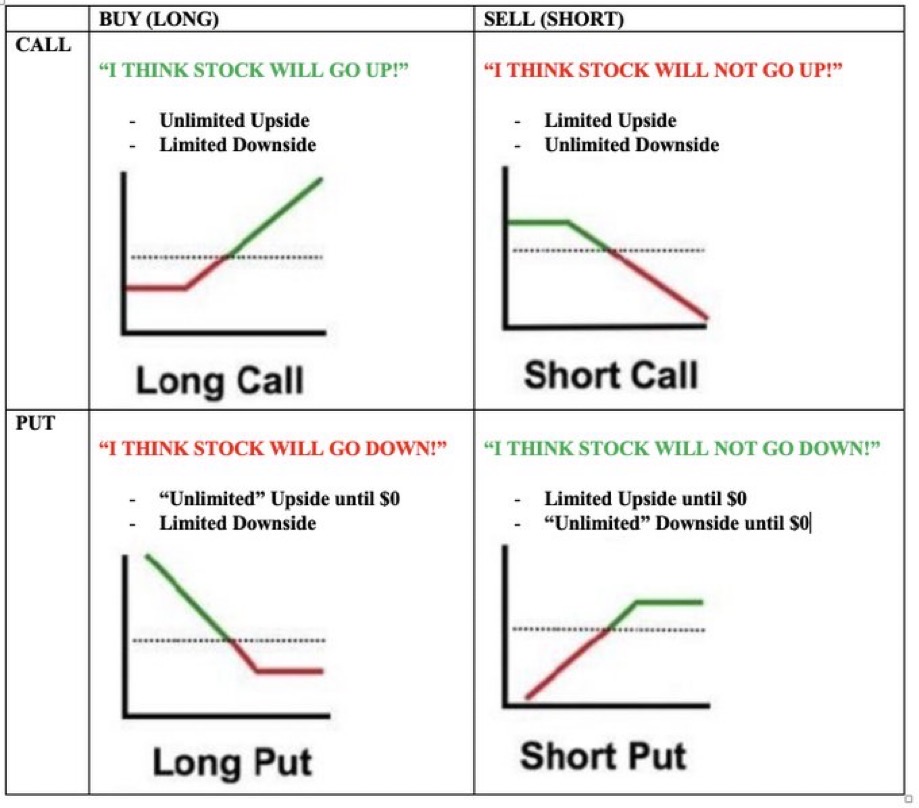

When you buy a call, you are bullish. Your risk is a premium you paid, and your profit potential is unlimited when the market goes up.

When you buy a put, you are bearish. Your risk is a premium you paid, and your profit potential is unlimited when the market goes down.

When you sell a call, you are bearish. Your risk is unlimited, and your maximum gain is the premium you received.

When you sell a put, you are bullish. Your risk is unlimited, and your maximum gain is the premium you received.

The thing about the option is that you can buy or sell more of them simultaneously to create multi-leg positions.

If you are still convinced of the direction, you can trade Call or Put spreads.

This means you are buying an option and also selling a less expensive option at the same time.

This limits your upside, but you also pay less premium for the option.

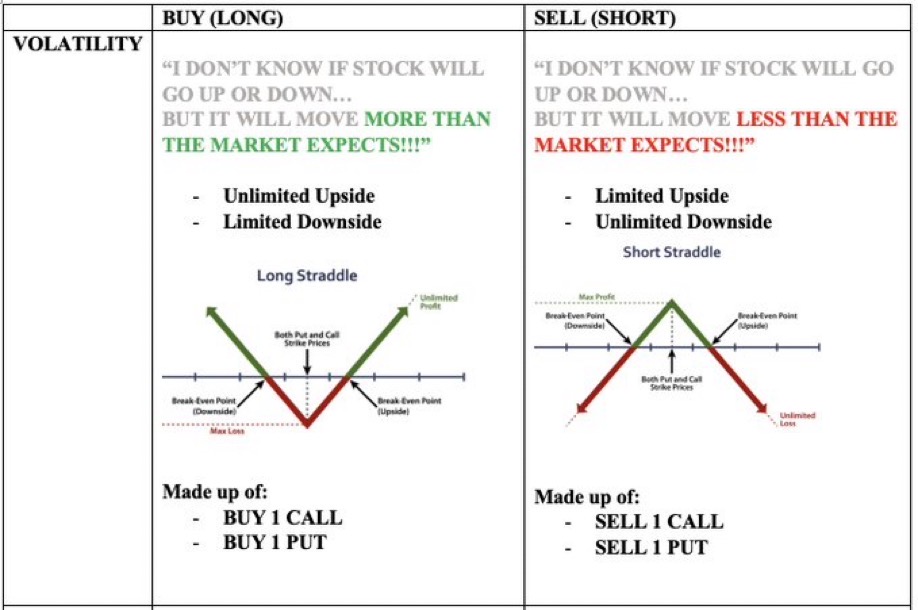

The last thing you can express with options trading is trading volatility.

Butterflies, Straddles, Strangles, Iron Condors and so on are different names for different options strategies that are used.

One of the examples is a Straddle.

When you buy a Straddle, you buy put and call at the same strike price. Thanks to that, you make money when the market goes either direction from your strike price. You are basically betting on volatility to come into the market soon.

When you sell a Straddle, you sell put and call at the same strike price. It is the opposite of buying straddle, and you don’t want any significant move to happen, and you make money thanks to time decay for your option to expire worthlessly, and you collect the premium.

There is a ton of options strategies, and it is way beyond the scope of this article to cover them; if you want to learn more about options overall, I recommend you pick up Option Volatility and Pricing by Natenberg or if you prefer more of a fun meme format Kamikaze Cash on youtube is an excellent channel for it.

Volatility

So if you got this far in the article and thought options are quite confusing, this is where the complicated part starts.

Once again, it is beyond the scope of this article to cover everything in detail, but I will try to give you just a brief overview of volatility and greeks.

So what is volatility?

Volatility refers to the fluctuation in the price.

In options, it reflects on the volatility of the underlying asset.

When the market is stable, it has lower volatility.

When the market experiences large swings in price, volatility is high.

The price of the option has three key factors.

- Intrinsic value

- Time value

- Volatility

The higher volatility is, the more expensive option is as it has more potential for movement.

There are two types of volatility you will see mentioned in the options space.

Historical Volatility

Historical (sometimes called statistical) volatility is a backward looking indicator that shows the volatility of underlying assets in the past.

This is a simple indicator that looks like any other oscillator.

Implied Volatility

Compared to Historical volatility, implied volatility is a forward-looking indicator and tells us what volatility we can expect in the future.

It is calculated by using standard deviation from the underlying asset.

Implied volatility increases with large price movements in the underlying, with increasing implied volatility options also get more expensive as the expected price range increases.

IV (implied volatility) usually increases before macroeconomic releases and decreases shortly after them.

in the IV, there is also an IV Rank that compares the current IV to values over the past year, and the IV percentile that represents the current IV relative to past values.

Although these two sound similar, the difference is that the IV percentile tells us a percentage of days over the past year that IV was below the current level.

The IV percentile of 80 means that IV was below the current level 80% of the time in the past year.

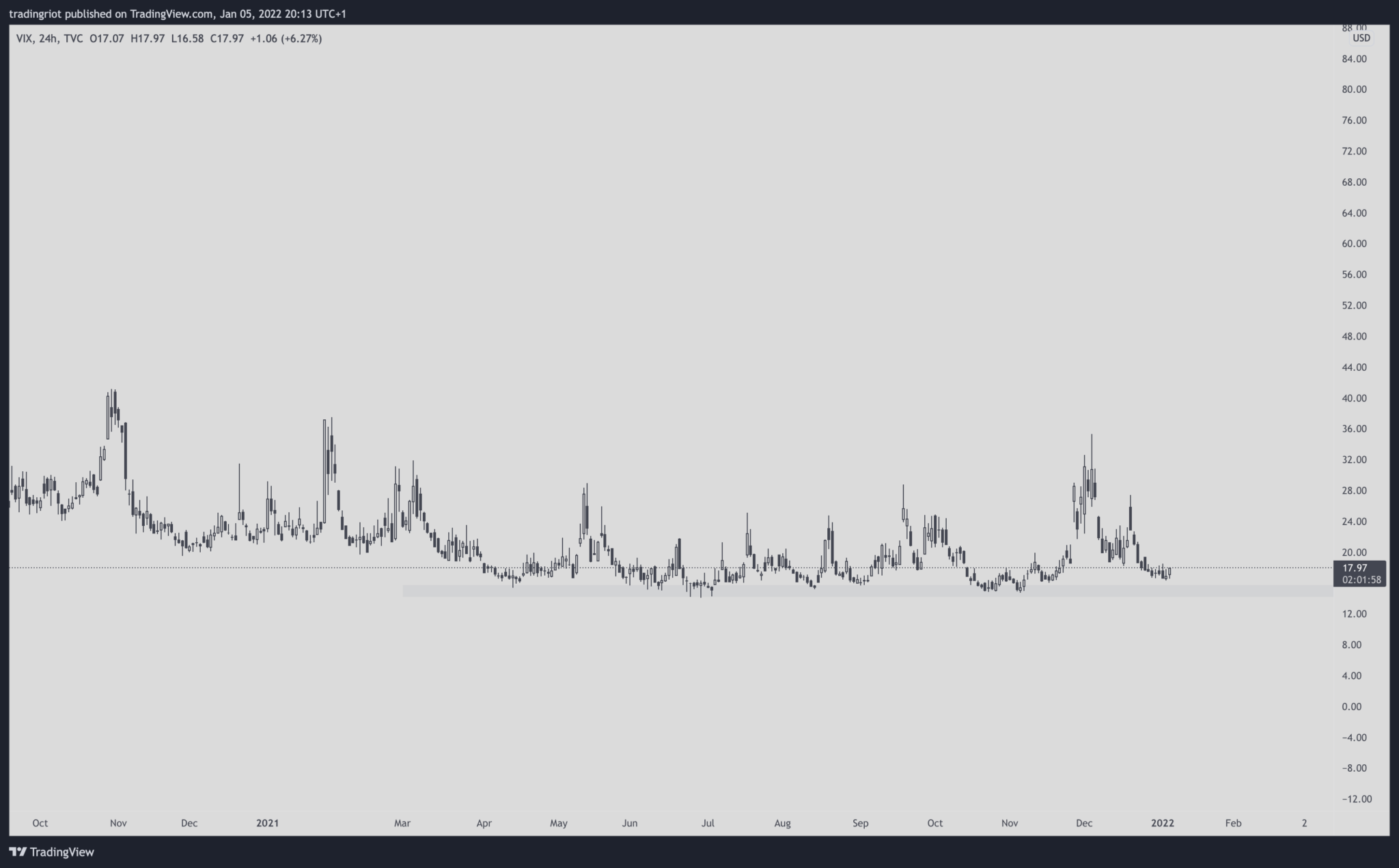

Volatility Index (VIX)

The CBOE (Chicago Board Options Exchange) created the Volatility Index (VIX) to measure the 30-day expected volatility of the US stock market.

The VIX is using real-time prices of S&P500 call and put options.

As you can see from the VIX chart, volatility tends to be mean-reverting, and periods of low volatility are followed by significant moves and vice versa.

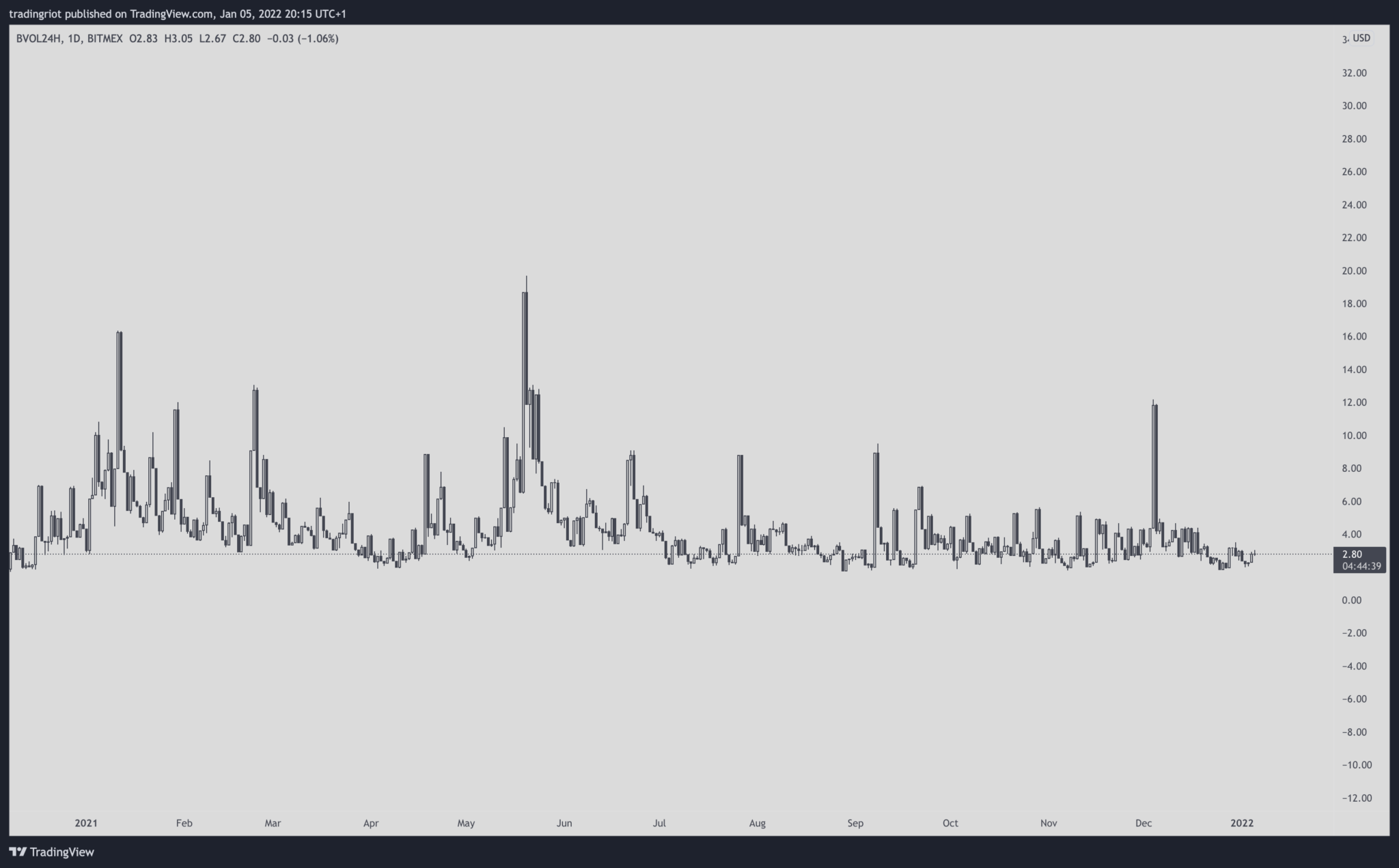

For Bitcoin, we can look at the BVOL index created by Bitmex, which is telling us the same thing.

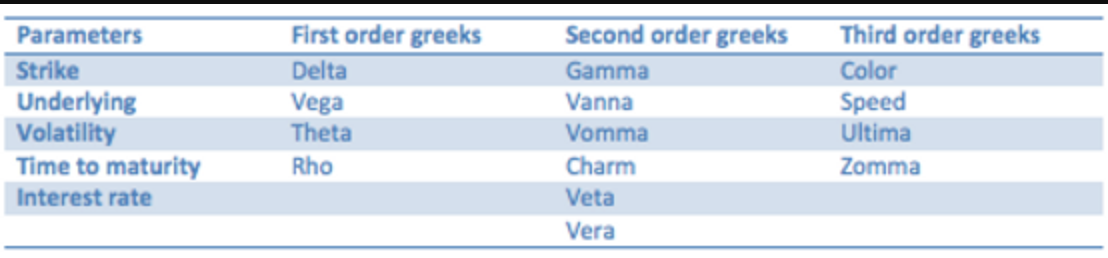

Greeks

You might have heard about greeks in the past.

Greeks represent variables that determine options price, which is constantly changing.

If you ever traded options, you might have encountered a situation where option price did not really correlate with underlying price, greeks will tell you why.

You will usually find greeks right at the options table.

As you can see, there are first order, second order and third order greeks.

In this article, we just stick to first-order greeks. Honestly, you don’t need to bother much with the second and third-order ones.

Delta

Amount of options price changes for $1 change in the underlying. Calls have Delta between 0 and 1. Puts have Delta between 0 and -1.

Gamma

Closely related to Delta, gamma is the rate of change in Delta for every $1 change in underlying.

Theta

Also known as time-decay, theta describes how the option’s value will change closer to expiration.

Vega

Amount of options price change for 1% change in IV

Rho

An option price sensitivity to interest rate changes

Non-Directional Trading Using Derivatives

Now you should have a decent understanding of derivatives.

In the last part of this article, I will take you through some strategies used in the markets but don’t rely on being correct if the underlying is going to go up or down.

Volatility trading

Thanks to options, you can trade volatility, and I already covered a little bit in this article.

You can either be long volatility or short volatility.

If you are long volatility, you are expecting a significant move to happen in the coming days; if you are short volatility, it’s the opposite.

Buying or selling a straddle is the most popular strategy for it.

You can use a chart of VIX or BVOL to see levels where the volatility usually bounces or short after a large price spike.

Move contracts

If you want to trade volatility in crypto and you don’t want to use options, you can use move contracts.

They are basically the same as straddles, and you can find them on exchanges such as FTX or Delta.

On FTX you will find daily, weekly and quarterly move contracts.

Daily move contracts expire to the absolute value of the difference between Bitcoins open and close price for a given day.

For example, if BTC opens the day at $40,000 and closes the day at $42,000, the daily move contract will expire with the value of $2000.

If BTC falls from $40,000 to $36,000, move contract will expire at $4,000.

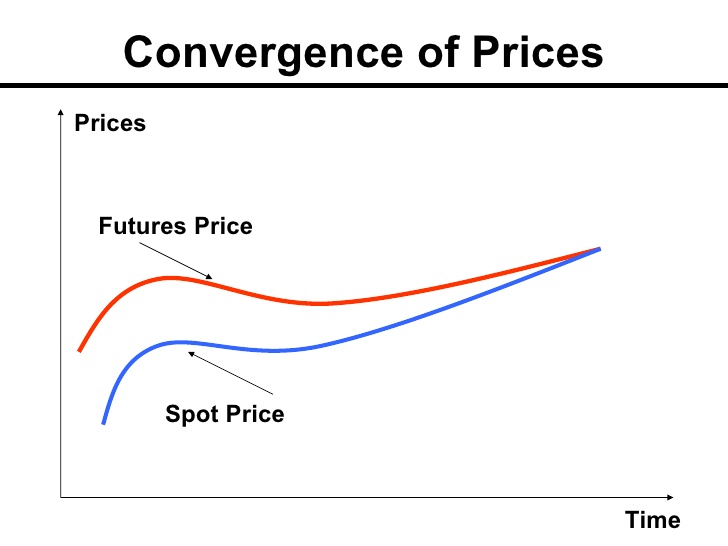

Cash and Carry

Cash and carry is an arbitrage type of trade that exploits imbalance between underlying and derivative, mostly futures with an expiration date.

In practice, this would mean you open a short on a futures contract that trades above the spot market price.

At the same time, you are also holding the same spot, this would create a delta neutral position, and you would profit on the difference between futures and spot as prices converge at the expiration.

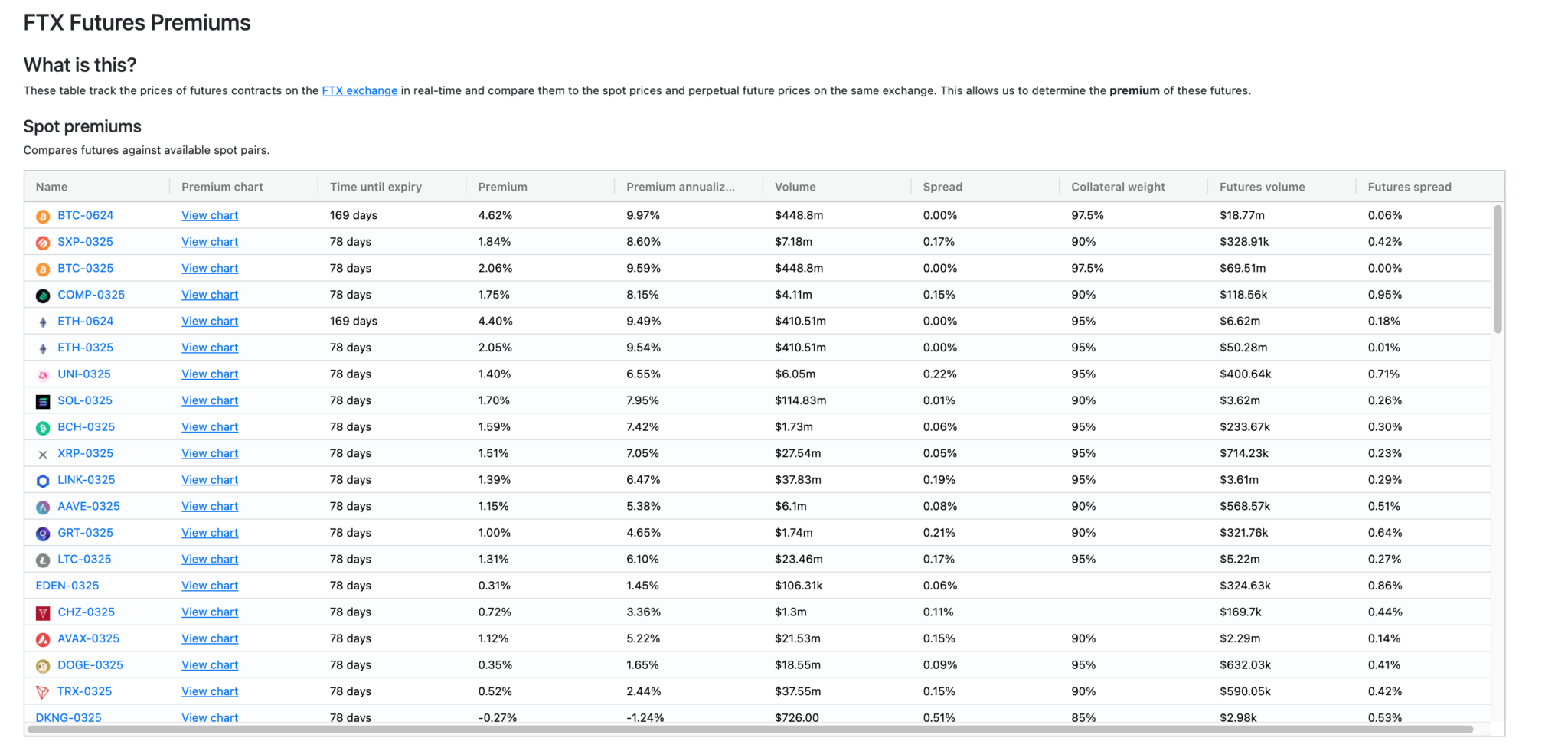

To track premiums and other interesting statistics in cryptocurrencies, you can use https://ftxpremiums.com/.

Premium in futures is correlated with overall market conditions.

In bullish trends, premiums rise, and in downtrends, they decrease.

Basis Trade

In cryptocurrencies, there are many ways to generate passive income by creating a delta neutral position that will generate some returns.

In this article, I will give one example of how trade could look like, but you will have to do the hard work.

These opportunities are usually in the Defi space, where volumes tend to be relatively low, and I don’t want to ruin those opportunities for those who take time to seek them.

If you go to https://mango.markets with is Solana based DEX, you can be short Mango-Perp and buy Mango at the spot market.

You would generate profit on this trade every hour thanks to the Funding rate.

As funding is positive you are getting paid 0.0087% every hour, which equals 75.78% in a year.

You need to bear in mind that this funding rate is going to change every hour, so you need to frequently look if it is worth it to hold the position open.

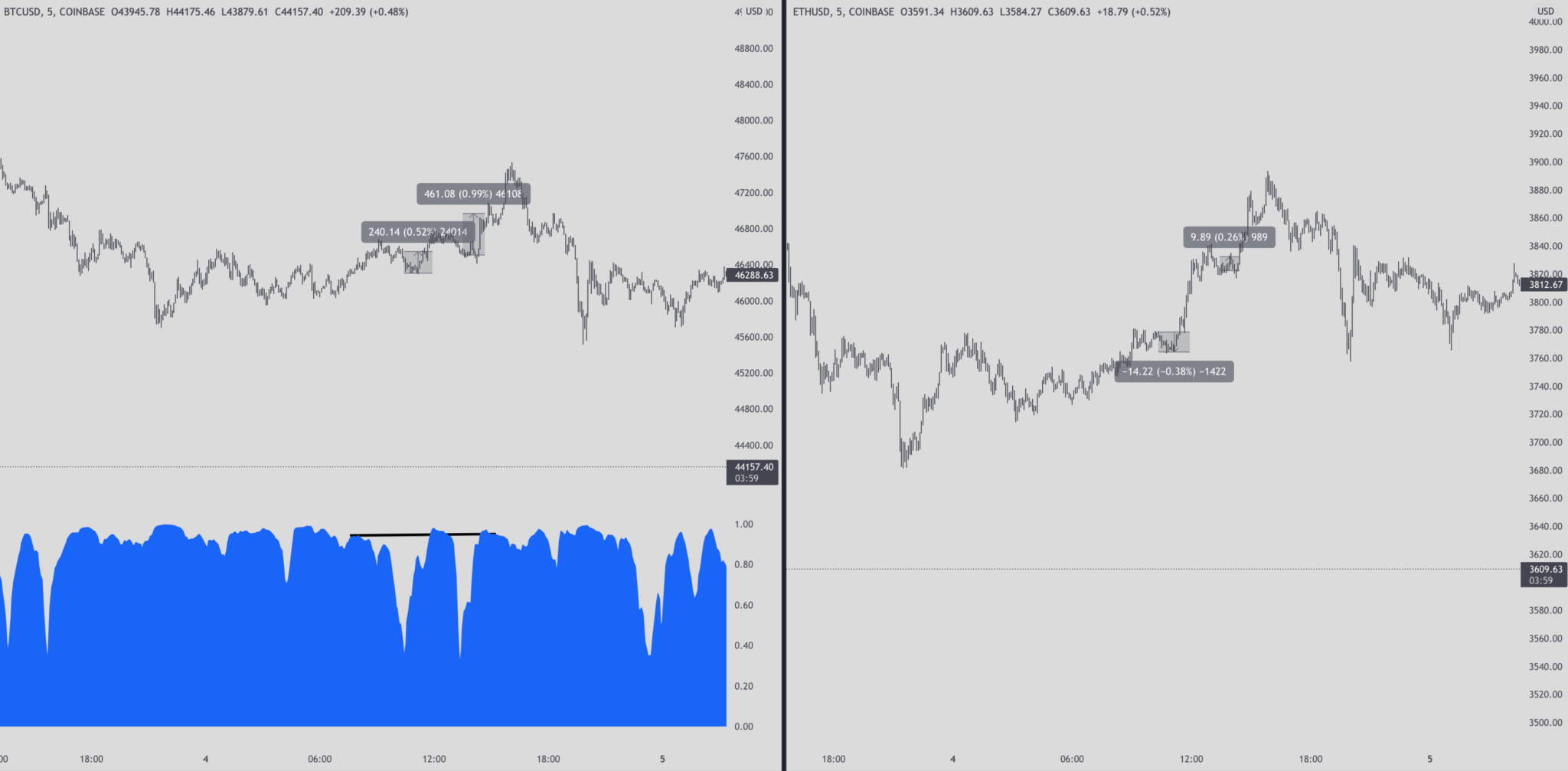

Pairs Trade

When you are pair trading, you are picking up two highly correlated assets and if their correlation breaks, you are betting on return in the future.

When correlation breaks, you take long in underperforming asset A and short it outperforming asset B until correlation is back to high numbers.

Bitcoin and ETH have a correlation of around .95 currently.

You can see that on January 4th, when correlation dipped toward .50, you could take long in BTC that was underperforming on a day and short in ETH that was outperforming.

BTC played a nice “catch-up” to ETH in both instances just minutes later.

Conclusion

The world of derivatives is huge, and it can be scary for those that lack an understanding of simple mechanics.

If you feel extra motivated to read another 900+ pages about derivatives, I recommend picking up this book from Hull.

I hope this article gave you at least a general understanding, and you will understand things you trade now a little bit better.

If you enjoyed the article, you could pick up the Trading Blueprint that demonstrates how I personally day trade futures.

Abdalla Musleh

Great explanation, clear and simple!! keep it up